Key Highlights

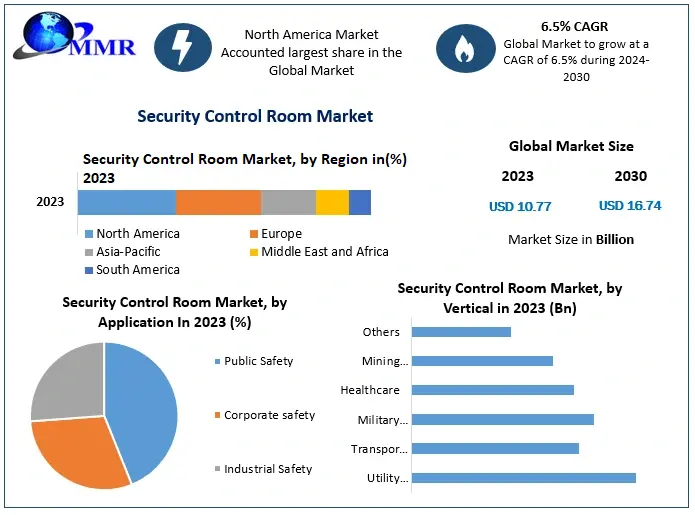

- Global Security Control Room Market was valued at USD 10.77 billion in 2023 and is expected to reach USD 16.74 billion by 2030, growing at a CAGR of 6.5%. Every percentage point of growth signals rising investment in centralized security operations and digital monitoring infrastructure.

- Real-time monitoring has emerged as the primary demand catalyst, increasing deployment of integrated surveillance, communication, and incident-response technologies.

- Smart city initiatives are expanding the role of control rooms beyond surveillance into traffic management, emergency coordination, and urban resilience programs.

- Artificial intelligence and machine learning are becoming core operational technologies, enabling automation, predictive analytics, and anomaly detection.

- Physical and cybersecurity convergence is reshaping security architectures across healthcare, utilities, transportation, and public-sector environments.

Why This Matters Now

The next wave of digital infrastructure investment is not occurring solely inside semiconductor fabs, AI data centers, or cloud platforms. It is increasingly happening inside security control rooms that serve as the operational nerve centers for cities, transportation systems, industrial facilities, and critical infrastructure.

As AI adoption expands, organizations generate larger volumes of surveillance video, sensor data, and operational intelligence. That surge creates demand for higher-performance processors, edge-computing systems, networking hardware, storage solutions, display technologies, and software platforms capable of delivering real-time situational awareness. The result is a growing intersection between security technology and the broader electronics and semiconductor ecosystem.

Get a sample of the report: https://www.maximizemarketresearch.com/request-sample/1505/

Market Overview

The Security Control Room Market is entering a modernization cycle driven by the need for continuous visibility, faster incident response, and integrated security management. The market reached USD 10.77 billion in 2023 and is forecast to achieve USD 16.74 billion by 2030. This expansion reflects growing reliance on centralized command environments that aggregate data from surveillance systems, access controls, communication networks, and operational technologies.

What changed is the scale of information entering these environments. Traditional control rooms primarily monitored video feeds. Modern control centers process data from cameras, sensors, access systems, connected devices, and digital security platforms simultaneously.

Why now? Organizations face a more complex risk environment. Physical threats, cyber threats, infrastructure vulnerabilities, and regulatory requirements increasingly overlap. Security leaders need unified operational visibility rather than isolated systems.

Key Trends Driving Growth

Artificial intelligence and machine learning are becoming foundational technologies in modern security operations. Security control rooms now use AI algorithms to analyze massive volumes of data, identify patterns, detect anomalies, and automate routine processes. This reduces operator workload while improving decision quality and response speed. The business implication is clear: organizations can scale monitoring capabilities without proportional increases in staffing.

Smart city development is creating another powerful growth engine. Municipal authorities are deploying integrated traffic systems, public safety networks, and emergency response frameworks that rely on centralized monitoring facilities. Security control rooms increasingly function as urban command centers, coordinating transportation, safety, and infrastructure management in real time.

The convergence of physical and cybersecurity is also reshaping investment priorities. Organizations are recognizing that cyber incidents can create physical consequences, while physical breaches can expose digital systems. Integrated control rooms provide a unified operating environment that supports comprehensive risk management and faster incident containment.

For electronics manufacturers, these trends translate into sustained demand for advanced displays, networking equipment, processors, storage platforms, communication systems, and intelligent software architectures.

Segment Insights

Based on the report's segmentation framework:

- Dominant Segment: Not specified in the published report source. The report segments the market by Offerings, Applications, and Verticals but does not publicly identify the largest revenue segment.

- Fastest-Growing Segment: Not specified in the published report source.

- Offering Segments: Hardware, Software, Services.

- Application Segments: Public Safety, Corporate Safety, Industrial Safety.

- Vertical Segments: Utility and Telecom, Transportation, Military and Defense, Healthcare, Mining and Manufacturing, and other sectors.

The strategic significance of these segments extends beyond security spending. Hardware demand supports electronics manufacturing ecosystems. Software adoption drives analytics and AI integration. Services accelerate recurring revenue models and long-term platform adoption.

Regional Growth Story

The report evaluates North America, Europe, Asia-Pacific, the Middle East and Africa, and South America as major market regions.

North America benefits from mature security infrastructure, extensive surveillance deployment, and advanced digital transformation programs. Organizations across government, healthcare, transportation, and critical infrastructure continue investing in integrated monitoring capabilities.

Asia-Pacific stands out due to accelerating urbanization and smart city development. Large-scale infrastructure projects create opportunities for integrated command centers that combine transportation monitoring, public safety, and emergency management functions. The region's growing electronics manufacturing base further strengthens the supply ecosystem supporting control room deployments.

Europe's focus on infrastructure resilience, regulatory compliance, and critical asset protection supports continued modernization efforts, while emerging economies increasingly view centralized command systems as strategic investments in public safety and operational efficiency.

Competitive Landscape

Competition is shifting from standalone hardware products toward integrated security ecosystems.

Technology providers that combine surveillance systems, AI analytics, communication platforms, and incident management software are gaining strategic advantages. The market is moving away from fragmented deployments toward unified operational environments capable of processing multiple data streams simultaneously.

The emergence of AI-enabled monitoring signals a broader transition toward software-defined security architectures. Vendors capable of integrating machine learning, automation, and predictive analytics are positioned to capture greater value than suppliers focused solely on hardware infrastructure.

For semiconductor suppliers, this transition is particularly significant. Advanced video analytics, machine learning workloads, edge processing, and real-time data correlation require increasingly sophisticated computing resources. As control rooms evolve into intelligence centers, demand for high-performance electronics will continue expanding across the value chain.

Recent Developments

- Integration of AI and machine learning technologies into security control room operations for advanced analytics and automated decision support.

- Growing deployment of integrated smart city command centers supporting traffic management and public safety coordination.

- Increased convergence of physical and cybersecurity management within unified control environments.

- Expansion of real-time monitoring capabilities through connected sensors, surveillance systems, and communication networks.

Strategic Implications

The market's evolution signals a broader transformation in operational intelligence.

Organizations are no longer investing in control rooms solely for security. They are investing in decision-making infrastructure. Control rooms increasingly support business continuity, operational efficiency, emergency management, and infrastructure resilience.

For electronics OEMs, this creates opportunities in display technologies, networking equipment, sensors, communications hardware, and intelligent monitoring platforms. For software providers, AI-enabled analytics and automation capabilities become key differentiators. For investors, recurring software and service revenues offer attractive long-term value creation opportunities.

The biggest beneficiaries are likely to be companies that can integrate physical infrastructure, cybersecurity capabilities, AI analytics, and real-time operational intelligence into a single platform.

Future Outlook

The next phase of market expansion will be defined by intelligent automation rather than surveillance expansion alone. Security control rooms are evolving into digital command centers that merge AI analytics, real-time monitoring, cybersecurity awareness, and operational intelligence into unified decision platforms. Organizations that build AI-enabled, integrated command environments will gain visibility, resilience, and response speed, while those relying on fragmented legacy systems risk falling behind in an increasingly data-driven security landscape.

Analyst Perspective

"The Security Control Room Market is moving beyond traditional surveillance toward intelligent operational command environments. Organizations are prioritizing real-time visibility, AI-powered analytics, and integrated security architectures to improve decision-making and resilience. The convergence of physical and digital security will remain one of the market's most influential growth catalysts over the forecast period." — Rucha Deshpande

About Maximize Market Research:

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research:

3rd Floor, Navale IT Park, Phase 2

Pune Banglore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656